Enabled by Government Failure to Allow Market Forces to Dictate Outcomes

Could Spirit Airlines Have Prevented Its 2026 Bankruptcy?

Spirit Airlines’ 2026 bankruptcy was not inevitable. The carrier could have avoided collapse only through early, decisive action targeting its structural weaknesses – unsustainable debt, rising fuel costs, grounded aircraft, and a deteriorating ULCC revenue model. As noted in the document, “Spirit Airlines could have avoided a 2026 bankruptcy only by attacking its structural weaknesses early: unsustainable debt, rising fuel costs, grounded aircraft, and a broken ULCC revenue model.”

The key forces driving Spirit’s failure included:

- Liquidity deterioration and mounting losses

- The blocked JetBlue merger, which eliminated the airline’s clearest path to scale

- Pratt & Whitney GTF engine groundings, which crippled fleet utilization

- Fare‑war pressure from legacy carriers matching ULCC pricing

These pressures exposed the fragility of the ULCC model and accelerated Spirit’s decline.

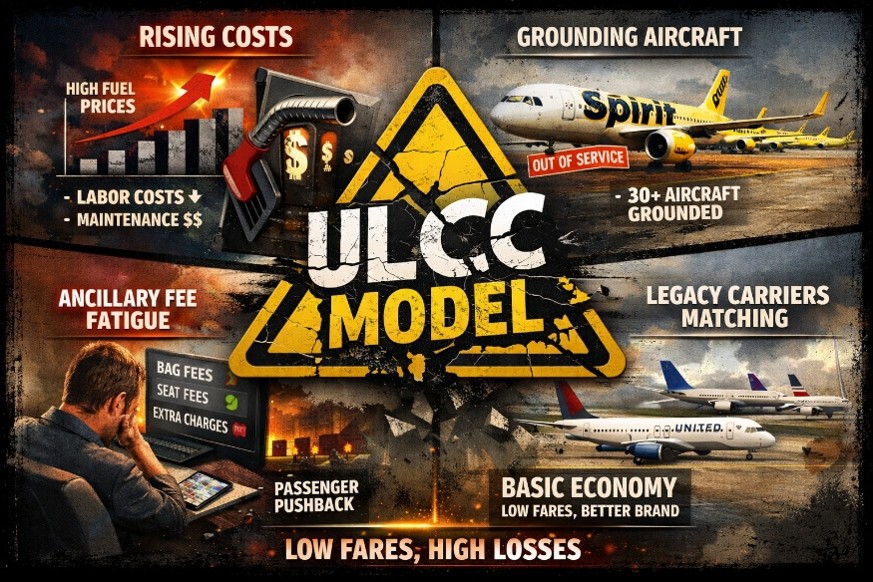

Why the ULCC Model Is Now Considered Structurally Broken

For more than a decade, the ULCC model – built on ultra‑low fares, high ancillary revenue, and extreme cost discipline – delivered strong load factors and reliable margins. As the document states, the model relied on “ultra‑low base fares to stimulate demand… high ancillary revenue… extreme cost discipline.”

By 2024–2026, however, the model failed under conditions it was never designed to withstand.

1. Cost Inflation Outpaced ULCC Efficiency Gains

Labor, fuel, maintenance, and engine‑related costs rose faster than ULCCs could offset through efficiency. Grounded aircraft destroyed utilization economics.

2. Ancillary Revenue Reached Its Ceiling

Passengers became resistant to fee proliferation. Frontier’s 2024 fee reductions signaled the end of the “stacked fee” era.

3. Legacy Carriers Neutralized ULCC Pricing Power

Basic Economy products from United, Delta, and American matched ULCC fares while offering superior networks and loyalty programs.

4. Fleet Reliability Eroded

Spirit’s A320neo groundings – 30+ aircraft at times – represented hundreds of thousands of dollars in daily lost revenue.

5. Consumer Preferences Shifted

Post‑pandemic travelers increasingly valued comfort, bundled fares, and reliability.

6. Serial Bankruptcies Exposed Systemic Fragility

Spirit’s two Chapter 11 filings in nine months demonstrated that the ULCC model, as historically executed in the U.S., is no longer economically viable.

In Plain Terms: Why the ULCC Model Broke

The ULCC model works only when carriers are:

- The lowest‑cost operators

- Able to charge fees customers will tolerate

- Operating fully utilized fleets

- Competing against higher‑fare incumbents

When costs rise and competitors match fares, the model collapses. As the document summarizes: “ULCCs can’t raise fares… can’t cut costs further… can’t rely on fees… can’t absorb shocks.”

What Actually Drove Spirit Toward Bankruptcy

Unsustainable Debt and Liquidity Collapse

Spirit entered 2024 with $7.4B in debt and negative operating cash flow. Losses accumulated across 2024 – 2025, and creditors ultimately declined further financing.

Blocked JetBlue Merger

The DOJ’s 2024 decision to block the $3.8B JetBlue acquisition removed Spirit’s last viable path to scale and capital.

Fuel Price Volatility

Jet fuel spikes disproportionately impacted ULCC margins.

Engine Groundings

GTF engine failures grounded large portions of Spirit’s fleet, eliminating revenue and undermining the ULCC utilization model.

What Spirit Could Have Done to Avoid Bankruptcy

1. Early, Radical Debt Restructuring (2023–2024)

Spirit needed to pursue:

- Aggressive refinancing before interest rates rose

- Accelerated sale‑leaseback optimization

- A pre‑emptive Chapter 11 filing to preserve liquidity

Incremental fixes were insufficient.

2. Accelerated Fleet Reliability Mitigation

Given known GTF engine risks, Spirit could have:

- Secured short‑term leased aircraft

- Negotiated accelerated engine replacement and compensation

- Wet‑leased capacity to protect network integrity

Mitigation was too slow.

3. Strategic Pivot Away from Pure ULCC Economics

A 2023 – 2024 shift toward premium seating, bundled fares, and higher‑yield leisure segments would have reduced fare‑war exposure.

4. Network Rationalization

Earlier actions could include:

- Eliminating chronically unprofitable routes

- Concentrating on high‑yield leisure hubs (FLL, MCO, DTW)

- Reducing mid‑week flying

- Prioritizing utilization over growth

These steps were taken only after bankruptcy.

5. Strategic Partnerships After the JetBlue Block

Spirit needed to rapidly pursue:

- Renewed merger discussions with Frontier

- Joint ventures in maintenance, training, or scheduling

- Equity partnerships with lessors or private capital

Operating independently was not viable.

What Would Have Saved Spirit

To avoid the 2026 bankruptcy, Spirit needed to:

- Restructure debt early

- Mitigate engine groundings aggressively

- Pivot away from pure ULCC economics

- Shrink the network before losses escalated

- Secure a strategic partner after the JetBlue block

All of these actions were available between 2023-2025-but executed too late.

For More Information

To learn more about our workshops and leadership programs, please provide:

- Name

- Address

- Organization

- Role

Submit your request to our team and we will follow up with upcoming session details.