The aviation management operations sector continues to face sustained turbulence driven by global political tensions, supply chain fragility, and rising cost pressures.

These forces are reshaping fleet strategy, workforce stability, and customer‑service performance across airlines, OEMs, MROs, ANSPs, and airport operators. The disruptions are no longer episodic—they represent a structural shift requiring long‑term operational resilience and governance recalibration.

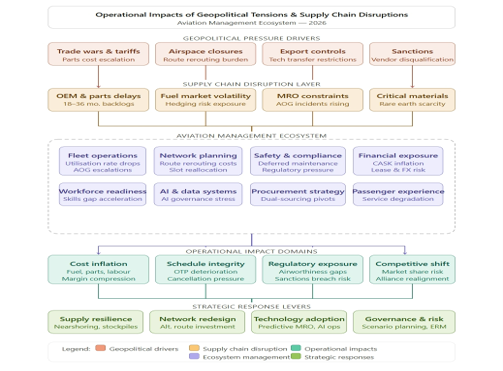

Geopolitical Tensions: A Persistent Operational Constraint

Global political instability is directly influencing aviation operations, procurement, and route economics.

Impacts

- Trade restrictions and tariffs continue to disrupt cross‑border flows of aircraft components, avionics, and raw materials.

- Titanium and specialty‑metal sourcing remains vulnerable due to geopolitical friction with major supplier nations, slowing aircraft production and certification timelines.

- Airspace restrictions in multiple regions are increasing flight times, fuel burn, and crew‑duty complexity.

- Regulatory divergence between major blocs (U.S., EU, China) is complicating certification pathways and slowing global fleet modernization.

Operational implication: Airlines and OEMs must plan for multi‑year volatility in material availability, routing constraints, and regulatory synchronization.

Supply Chain Disruptions: A Multi‑Billion‑Dollar Drag on Performance

The aviation supply chain remains one of the slowest‑recovering industrial ecosystems.

Current State

- Global aircraft backlogs exceed 17,000 units, delaying fleet renewal and forcing extended use of aging aircraft.

- Engine manufacturers face multi‑year maintenance queues, driving up leasing and spare‑engine costs.

- Parts shortages continue across avionics, interiors, landing‑gear components, and composite structures.

Cost Exposure

Industry estimates for 2025–2026 indicate more than $11 billion in additional operating costs driven by:

- Fuel inefficiency from older aircraft remaining in service.

- Maintenance escalation, including longer shop visits and higher material costs.

- Engine leasing premiums, up 20–30% since 2019.

- Inventory stockpiling, now a normalized risk‑mitigation strategy.

Operational implication: Airlines must balance capital discipline with the need to secure parts, engines, and maintenance capacity in an increasingly competitive environment.

Workforce Impact: Capacity Constraints and Rising Labor Costs

Labor shortages remain acute across pilots, technicians, dispatchers, and supply‑chain specialists.

Key Dynamics

- Technician shortages are extending maintenance turnaround times and increasing out‑of‑service rates.

- Pilot hiring competition is driving wage inflation and reshaping regional‑carrier economics.

- OEM and MRO labor gaps are slowing production and repair cycles, compounding supply chain delays.

- Burnout and attrition among frontline staff are rising due to operational irregularities and customer‑service pressures.

Operational implication: Workforce strategy must shift from recruitment‑focused to capability‑focused, emphasizing retention, cross‑training, and automation‑supported workflows.

Customer Service Degradation: The Downstream Effect

Passengers are experiencing the operational strain directly.

Observable Trends

- Record load factors (above 83%) are reducing schedule flexibility and increasing disruption sensitivity.

- Aging cabins and delayed interior retrofits are widening the gap between brand promise and passenger experience.

- Higher fares reflect rising fuel, maintenance, and leasing costs.

- More frequent delays and cancellations stem from aircraft availability issues and extended maintenance cycles.

Operational implication: Customer‑experience recovery will require coordinated action across fleet planning, staffing, and service‑delivery models—not just frontline improvements.

Strategic Imperatives for 2026 and Beyond

To navigate this environment, aviation leaders must prioritize industrial resilience and operational integration.

Focus Areas

- Diversify supply chains across regions to reduce geopolitical exposure.

- Accelerate predictive maintenance and digital‑twin adoption to mitigate aging‑fleet risks.

- Strengthen workforce pipelines through partnerships with technical schools, military transition programs, and cross‑sector training.

- Rebuild customer‑service resilience through schedule integrity, proactive communication, and operational transparency.

– Enhance governance frameworks to align risk, operations, and financial planning across the enterprise.

Information on upcoming workshops

Visit: www.leaders-hive.com